Comparison Summary

Comparison SummaryWe love Mercury as our business banking solution, that said, if you're looking for the best expense management software, you should check out our BILL Spend & Expense vs Ramp comparison instead.

Mercury has some expense management features, but pale in comparison to what BILL S&E and Ramp have out of the box. Even if Mercury had feature-parity, we would still use it alongside BILL or Ramp.

Business Banking

Business Banking MercuryBest

MercuryBestBest modern bank for SMB's and startup founders

Best modern bank for SMB's and startup founders Ramp

RampBest if you've limited banking needs and already using Ramp

Best if you've limited banking needs and already using Ramp

Expense Management

Expense ManagementBilling & Invoicing

Billing & InvoicingComparison Videos

Comparison VideosWhy We Switched to Mercury (After Testing Every Business Bank)

Why We Switched to Mercury (After Testing Every Business Bank) 8:47

8:47Why We Switched to Mercury (After Testing Every Business Bank)

Why We Switched to Mercury (After Testing Every Business Bank) 12:03

12:03The Startup Finance Stack I Use as a Founder

The Startup Finance Stack I Use as a Founder 16:58

16:58THE Complete Software Stack Every Small Business Needs 🤫

THE Complete Software Stack Every Small Business Needs 🤫Editor's Verdict

Editor's VerdictSafety & Protection

Safety & ProtectionMercury gives you real, proactive control over your money. You can block, approve, or limit any ACH pulls before they touch your account, so nothing gets taken without your explicit okay. If something looks suspicious, it's stopped cold and flagged before any funds move. That level of control is rare and means you're not just reacting to problems, you're preventing them.

Ramp spreads your deposits across multiple FDIC-insured banks like Mercury, so you're still covered for multimillion-dollar balances. But their ACH controls aren't as tight. If you require approval for a debit, the transaction can still hit your account first and only gets reversed if you act in time. So, you're always a step behind, not ahead.

If you care about actually blocking unauthorized transfers before they happen and want the strongest deposit protection, Mercury is the clear pick. Ramp is decent for expense management, but on real banking safety, it just doesn't match Mercury's level of control or peace of mind.

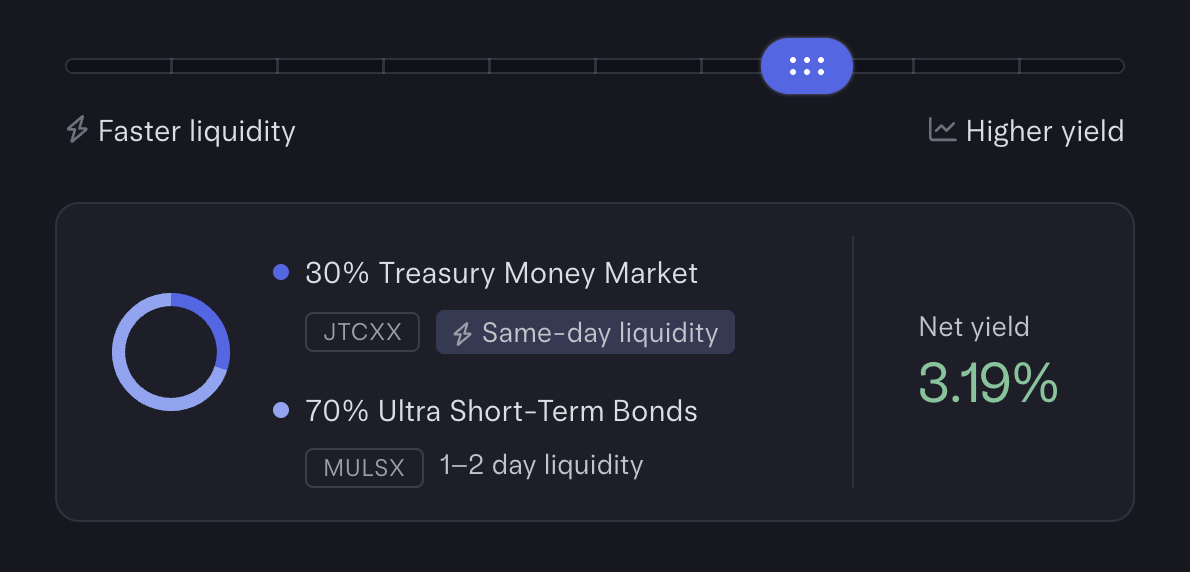

Earning Interest

Earning InterestMercury Bank makes earning interest on idle cash feel seamless, almost like using a regular savings account. The Treasury options are built right into the core banking experience, with automatic transfers and flexible liquidity choices, so you can easily optimize returns without complicating your daily cash flow.

Ramp technically lets you earn yield too, but it treats treasury features as more of an add-on than a core part of banking. The experience isn't as smooth or integrated, so managing interest on idle funds takes more effort and doesn't feel as natural.

If earning interest easily and keeping your cash working for you is a priority, go with Mercury. Ramp can do the job, but it's not built around this workflow and feels secondary. Mercury is the clear pick here.

Money Movement

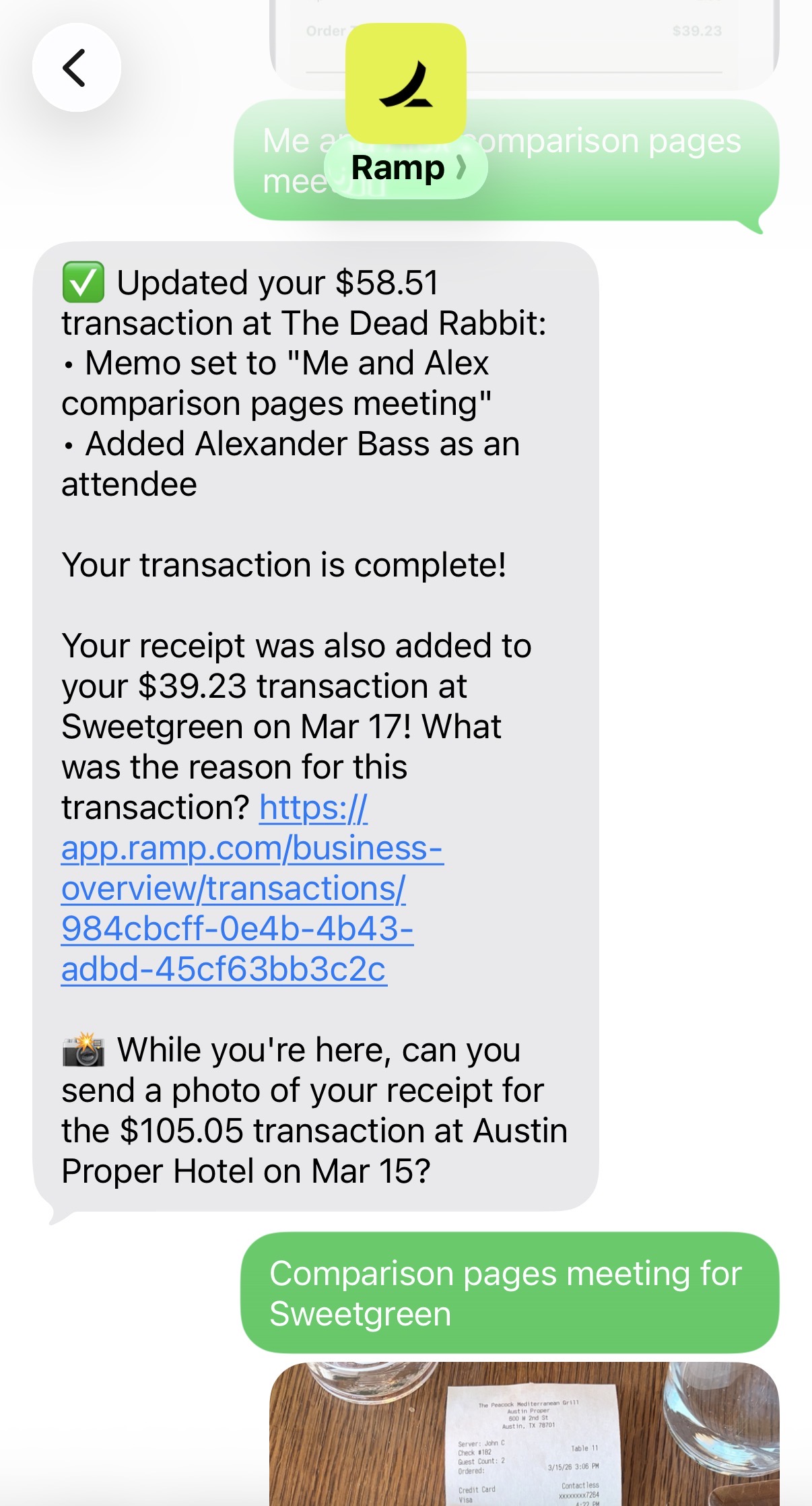

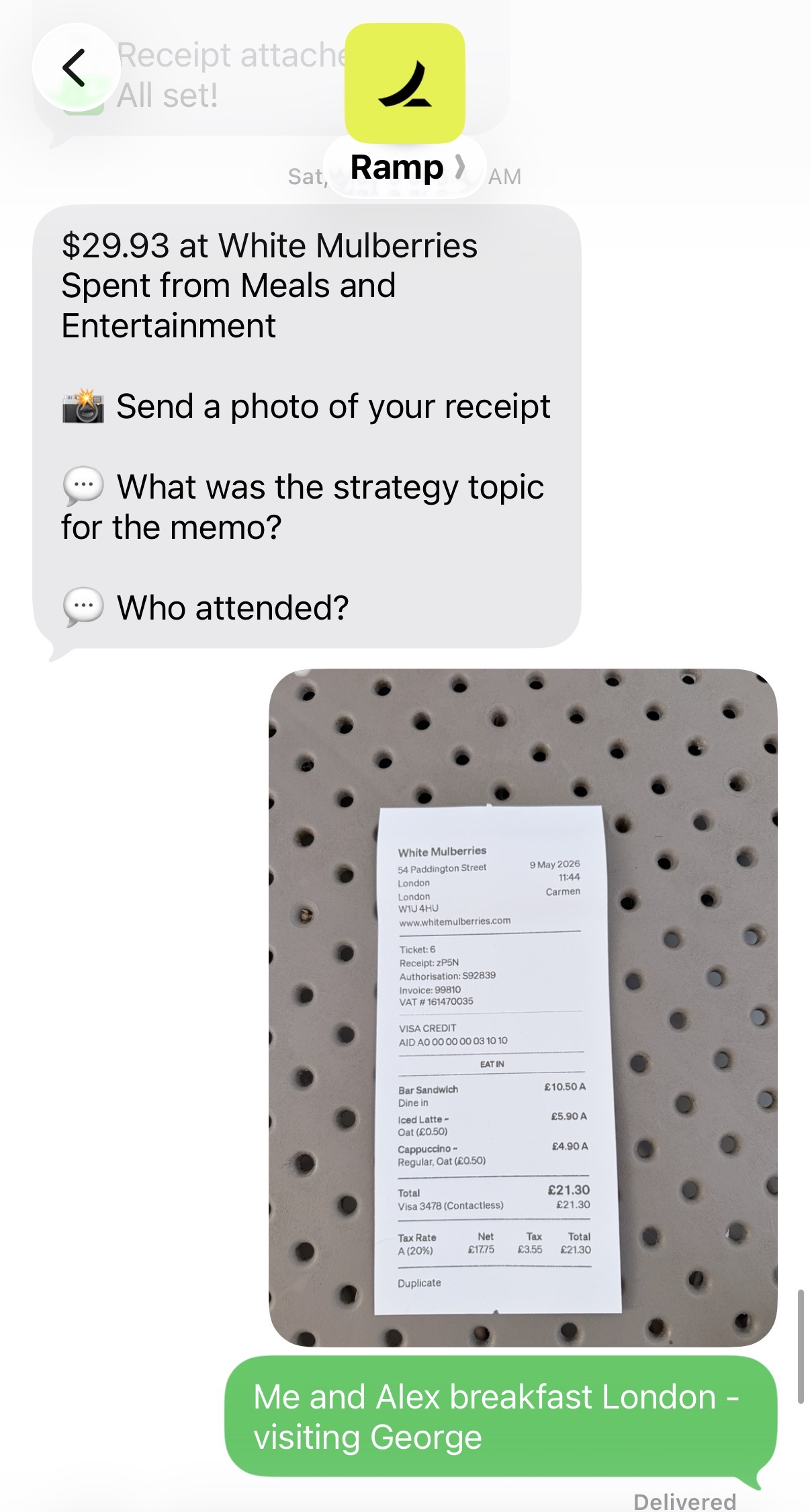

Money MovementMercury makes moving money feel almost effortless. Vendor onboarding, tax info collection, and payments are all handled in one place, with automatic W-9 requests and 1099 tracking built right in. You can send vendors a secure form, let them enter their details, and pay them by ACH or wire in just a couple clicks. Checks are handled for you, too, just upload your docs and Mercury prints and mails them with attachments. Invoicing is smooth and lets you accept payments through multiple methods, all trackable from your dashboard.

Ramp covers the basics like ACH, wires, checks, and vendor payments, but falls short when you need deeper banking features. Things start to break down if you want everything tightly integrated, especially with newer accounting software. Ramp's integrations tend to focus on credit card functionality and not the full suite of invoicing and bill pay you'd expect from a bank. That's why most teams end up pairing Ramp with a real bank like Mercury, rather than using it solo for money movement.

If you want money movement to actually save you time and headaches, especially around onboarding vendors and tax paperwork, Mercury is in a totally different league. Ramp can handle simple payments, but Mercury is the one that truly takes the pain out of the whole process. Go with Mercury if this stuff matters to you.

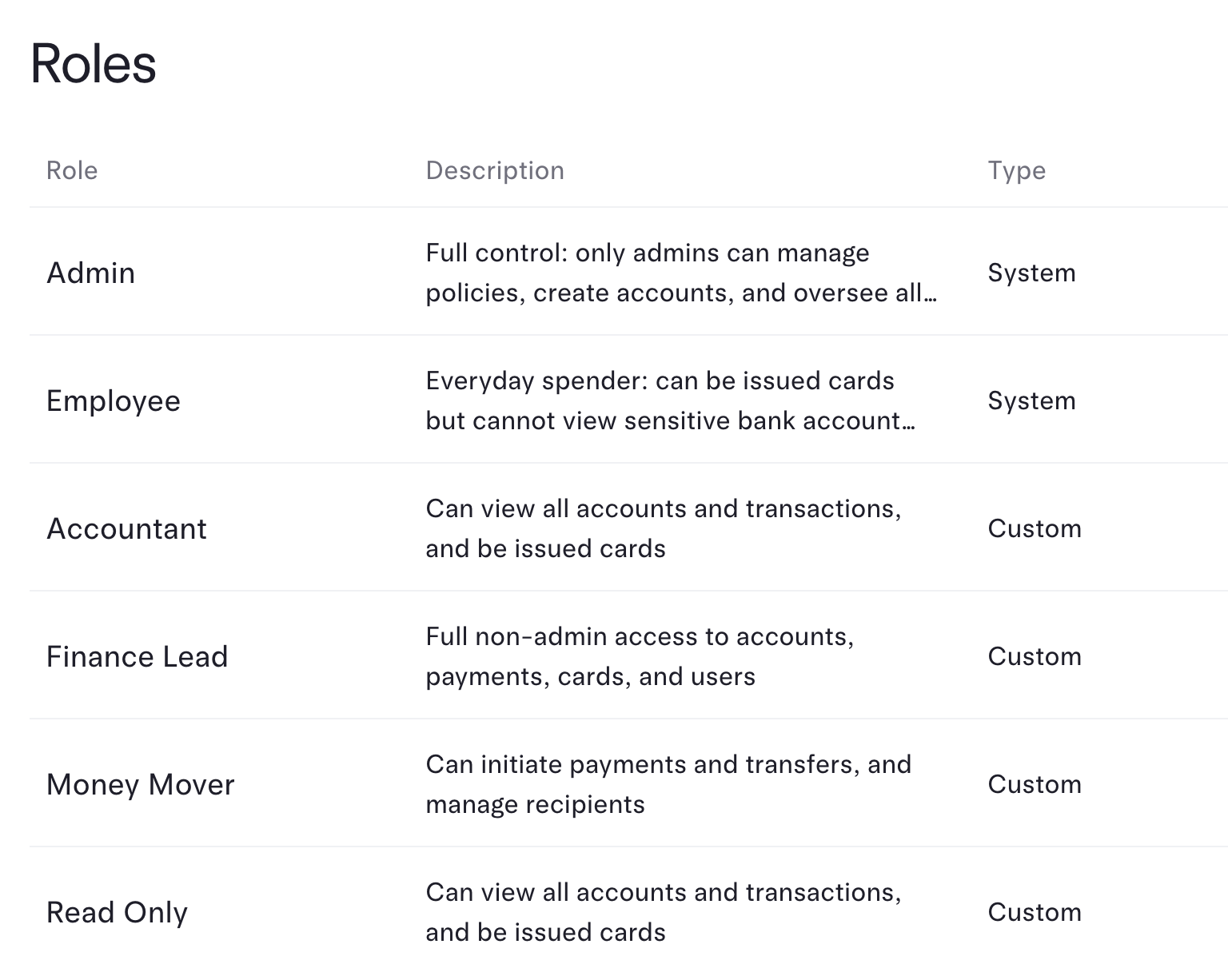

Organization & Controls

Organization & ControlsMercury absolutely blows Ramp away on organizing funds and controlling how money moves. You get up to 100 checking and 100 savings accounts per business, each with its own debit or credit card if you want, plus powerful auto-transfer rules that let you split deposits by percentage or keep target balances topped up automatically. It handles complex needs like approval workflows, dual admin controls, and granular user roles, right down to picking who approves big payments. You can even toggle between personal and business accounts with one login, and give employees free personal accounts if you want.

Ramp lets you open multiple business accounts and set up some roles, but all cards pull from the same pot and you can't set up real sub-accounts with their own cards or do detailed auto-transfers by category. Its automations are just about maintaining minimum or maximum balances, not actually splitting funds. Approvals only work on payments you send through Ramp, and you can't set rules that apply to all transfers or all accounts. There's no personal banking at all.

If you care about structuring company money across accounts, automating how cash moves, or setting up true guardrails, Mercury is in a completely different league. Ramp is decent for basic controls but stops short of what you'd need if you want deep organization and real banking rules. Go with Mercury if this stuff matters to you.

User Experience

User ExperienceMercury is in a different league for banking user experience. The interface is called out as "one of the best I've ever seen", modern, intuitive, and so smooth that loyal users refuse to switch. Everything feels built around clarity and speed.

Ramp is clean and modern, and the universal search is genuinely helpful, but you can tell banking isn't its main thing. Most of the interface is focused on expense management, and the banking parts feel like an add-on.

If you care about a banking interface that's actually designed for banking, fast, clear, and just a joy to use, Mercury is the obvious pick. Ramp's UX is solid for what it is, but it just doesn't compete here.

Screenshots

Screenshots

Ramp