Comparison Summary

Comparison SummaryYou can't go wrong with either BILL S&E or Ramp for virtual credit cards and expense management.

If you're a small business or have less cashflow, then BILL is your best bet as Ramp requires at-least 25K in your business bank (with your limit directly tied to this, so we really recommend you have $50–100K minimum in your account).

The most simple way to put it is, if you're a small business, use BILL S&E, if you're a startup with millions in the bank or mid-market, use Ramp.

Expense Management

Expense Management RampBest

RampBestBest for startups and tech-forward businesses

Best for startups and tech-forward businesses BILL Spend & ExpenseBest

BILL Spend & ExpenseBestBest for small businesses

Best for small businesses

Billing & Invoicing

Billing & InvoicingComparison Videos

Comparison VideosTHE Complete Software Stack Every Small Business Needs 🤫

THE Complete Software Stack Every Small Business Needs 🤫 16:58

16:58THE Complete Software Stack Every Small Business Needs 🤫

THE Complete Software Stack Every Small Business Needs 🤫 13:10

13:10Best Expense Management Software: Ramp vs Brex vs BILL Spend & Expense vs Expensify

Best Expense Management Software: Ramp vs Brex vs BILL Spend & Expense vs ExpensifyEditor's Verdict

Editor's VerdictSo you're looking for an expense management solution and you're deciding between BILL Spend & Expense (formerly Divvy) and Ramp. Well, we've used both and we're here to to tell you, they are both great options but there is a clear way to decide which one is right for you 👀

Ramp vs BILL Similarities

As a baseline, both Ramp and BILL offer virtual and physical corporate cards, that offer rewards, spend management tools, and have no annual fees. They both have card controls (budgets), spend tracking, and will allow you to spin up new employee cards within seconds (or cancel them just as quickly 😄). When integrated with Quickbooks Online, they will also both allow you to automatically reconcile your books.

Ramp vs BILL Differences

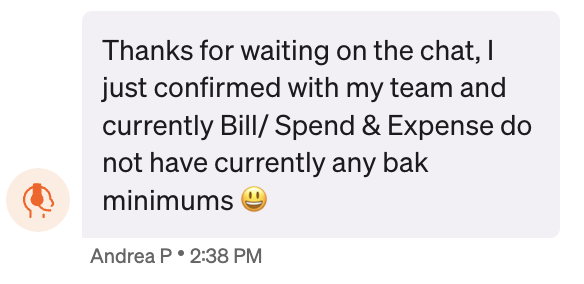

Bank Minimums

The size of your business makes a difference in terms of which expense management platform you choose. While both Ramp and BILL are free to use, they have different minimum bank bank balances in order to get approved for an account.

BILL Spend & Expense Bank Minimum: $0

Ramp Bank Minimum: $25,000

Even though Divvy was acquired by Bill, they still maintain $0 bank minimums to get approved for an account.

So an easy decision can be made—do you currently have $50,000 in your bank account? If not, stop your research and opt for BILL Spend & Expense.

Business Size

If it's not clear from the bank minimum requirements, Ramp is targeting slightly larger companies than BILL. If you're under 10-20 employees, BILL is likely more suited for you. If you're are larger team, or a start-up who just raised money looking to scale, Ramp is likely better for you.

Insights

This is where Ramp really shines. Ramp can send you data on duplicate spending and cost saving opportunities with different vendors. It can alert you if you have two people paying for the same service, for example. If you're a start-up, scaling company, or have many employees, Ramp would be best for you.

Credit Card Rewards

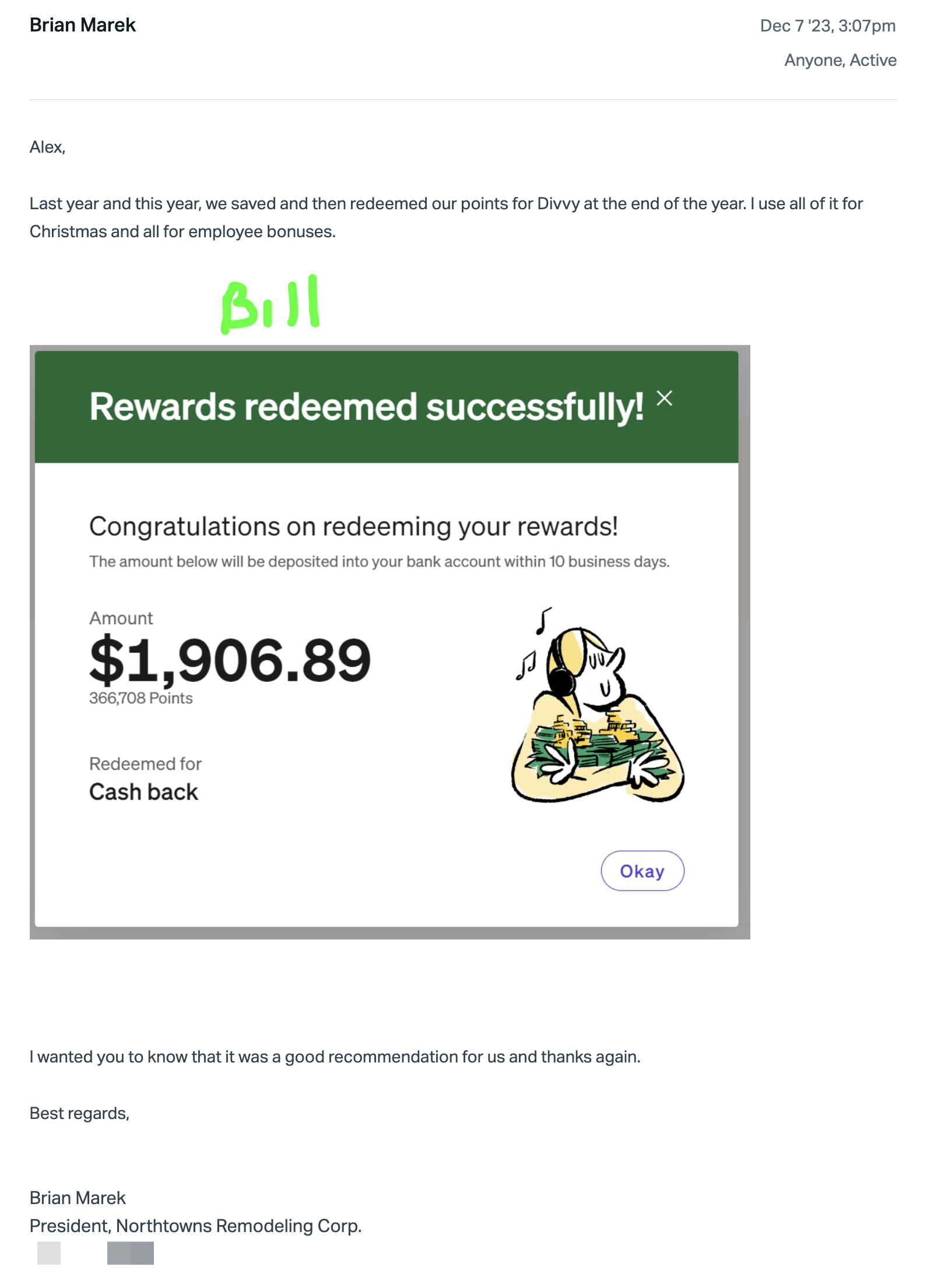

Ramp provides a straightforward 1.5% cash back on all purchases, while BILL offers up to 7x points on specific categories like restaurants and hotels. With BILL, the rewards are better if you pay your balance off weekly (vs semi-monthly or monthly), so we recommend doing that to optimize your cash back.

Quick story—about two years ago we introduced a small construction company (<10 person team) to BILL. The owner decided to use the cash back at the end of the year as a Christmas Bonus for his employees. This was "found money" that he wouldn't have otherwise had.

This construction company uses it's cash back for employee bonuses each year.

What would we choose?

Years ago, one of our clients asked if he could pay an invoice through Divvy (now BILL Spend & Expense). Upon looking into it, we realized just how awesome the platform was and decided we needed to use it for ourselves. There was no bank minimum, it was totally free, and we got rewards on our spending, AKA It was a no-brainer.

Upon researching other similar solutions on the market, we came across Ramp, and with the $25K bank minimum ($75K bank minimum at the time, which they seem to be reducing), it was something that our business just didn't have at the time.

So the decision was made many years ago and we're still using BILL Spend & Expense today.

That said, as our business grew and we had $50–100K in our bank account, we decided to apply for a Ramp account, knowing we'd probably love it. And the truth is, we did 😬

They have a beautiful UI and friendly UX, and offer cool insights into your spending. But at this point, the switching costs for us would be ultimately too high to even consider swapping to Ramp.

So we'll leave you with this, if you can meet the minimum bank requirements, give Ramp a shot (it's probably what we'd do). If you can't, don't fret—BILL Spend & Expense is an awesome choice!

Screenshots

Screenshots

Ramp