Comparison Summary

Comparison SummaryMercury Bank has a more modern banking experience with top-notch QuickBooks Online integration, great UI, and a strong feature set, while Novo frustrated me with clunky integrations and felt limited for anything beyond very small businesses.

Only use Novo if you're a freelancer or solopreneur with a small account and can't use Mercury Bank for some reason.

MercuryBest

MercuryBestBest modern bank for SMB's and startup founders

Best modern bank for SMB's and startup founders Novo

NovoSimple and least powerful

Simple and least powerful

At a Glance

At a GlanceComparison Video

Comparison VideoWhy We Switched to Mercury (After Testing Every Business Bank)

Why We Switched to Mercury (After Testing Every Business Bank) 8:47

8:47Why We Switched to Mercury (After Testing Every Business Bank)

Why We Switched to Mercury (After Testing Every Business Bank)Editor's Verdict

Editor's VerdictSafety & Protection

Safety & ProtectionMercury is in a totally different league for safety and protection. You get multi-bank FDIC coverage up to $5M, not just the standard $250K, and your money is automatically spread out so you're protected even if a bank fails. Plus, Mercury gives you real control over ACH pulls, you decide what moves out, nothing happens without your approval, and suspicious activity is flagged before any cash leaves. That's a huge deal if you want to avoid your account getting drained just because someone has your numbers.

Novo, on the other hand, is bare bones here. You get basic FDIC coverage at one bank, and if someone has your account details, they can pull money unless you notice and dispute it after the fact. It's really only set up for people with small balances who don't need extra layers of protection.

If safety and control matter at all, Mercury is the obvious pick. There's just no comparison, Novo doesn't come close.

Earning Interest

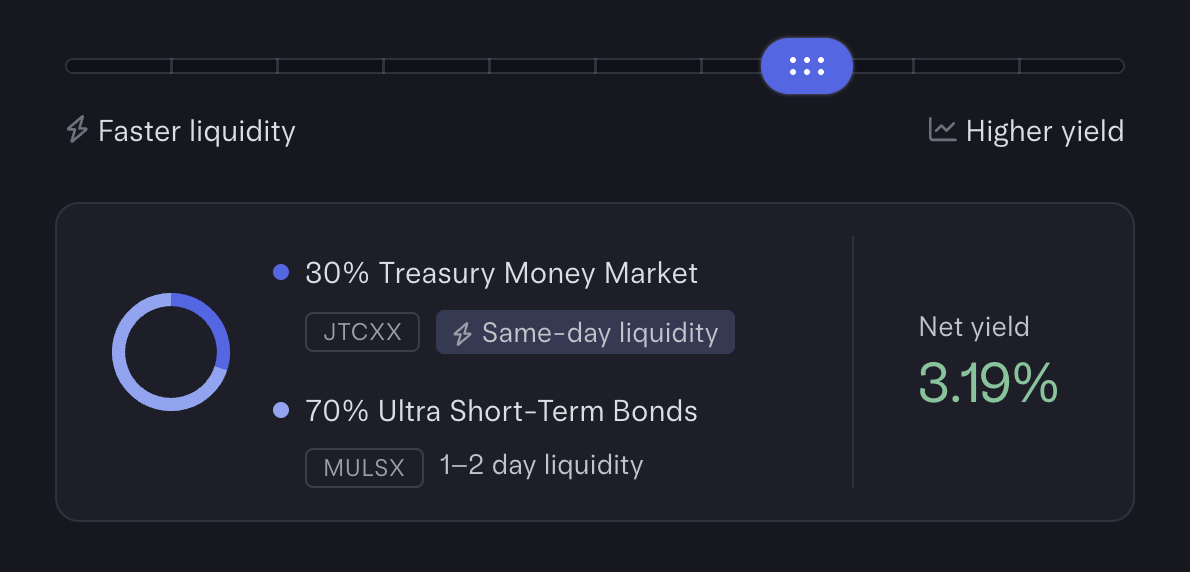

Earning InterestMercury Bank actually lets you earn interest on your idle cash with built-in Treasury options, while Novo gives you zero options for earning anything on your balance. Novo is just a plain checking account with no savings or investment features, so your money just sits there doing nothing.

With Mercury, you can set up automatic transfers to Treasury accounts, keep your cash working for you, and still access funds quickly when you need them. You get both higher yields and the flexibility to move money back to checking as needed, which makes managing idle cash effortless.

If earning interest on your business funds matters at all, Mercury is the clear pick. Novo just doesn't offer anything in this area.

Money Movement

Money MovementMercury gives you real vendor onboarding with secure forms, automatic W-9 collection, and keeps all the tax paperwork in one spot, which saves a ton of time if you pay contractors or have a growing team. Novo doesn't offer self-service onboarding or automatic W-9s, so you're stuck doing a lot of manual admin, which quickly gets messy as your business grows.

Sending checks is also way smoother with Mercury. You can attach up to six pages, including forms or invoices, and Mercury handles the rest. Novo will mail checks for you, but if you need to include any attachments, you're out of luck and have to find another way. That's a headache, especially for government forms.

Wire transfers are cheaper on Mercury too, with no fees for domestic or USD international wires, while Novo charges for outgoing domestic wires and passes on Wise's fees for international ones. On top of that, Mercury's invoicing flow is cleaner and actually enjoyable, while Novo's feels clunky and basic.

Unless you're a solo freelancer who never needs to pay others or deal with tax paperwork, Mercury is the obvious pick for money movement. Novo just can't keep up if you need anything more than the basics.

Organization & Controls

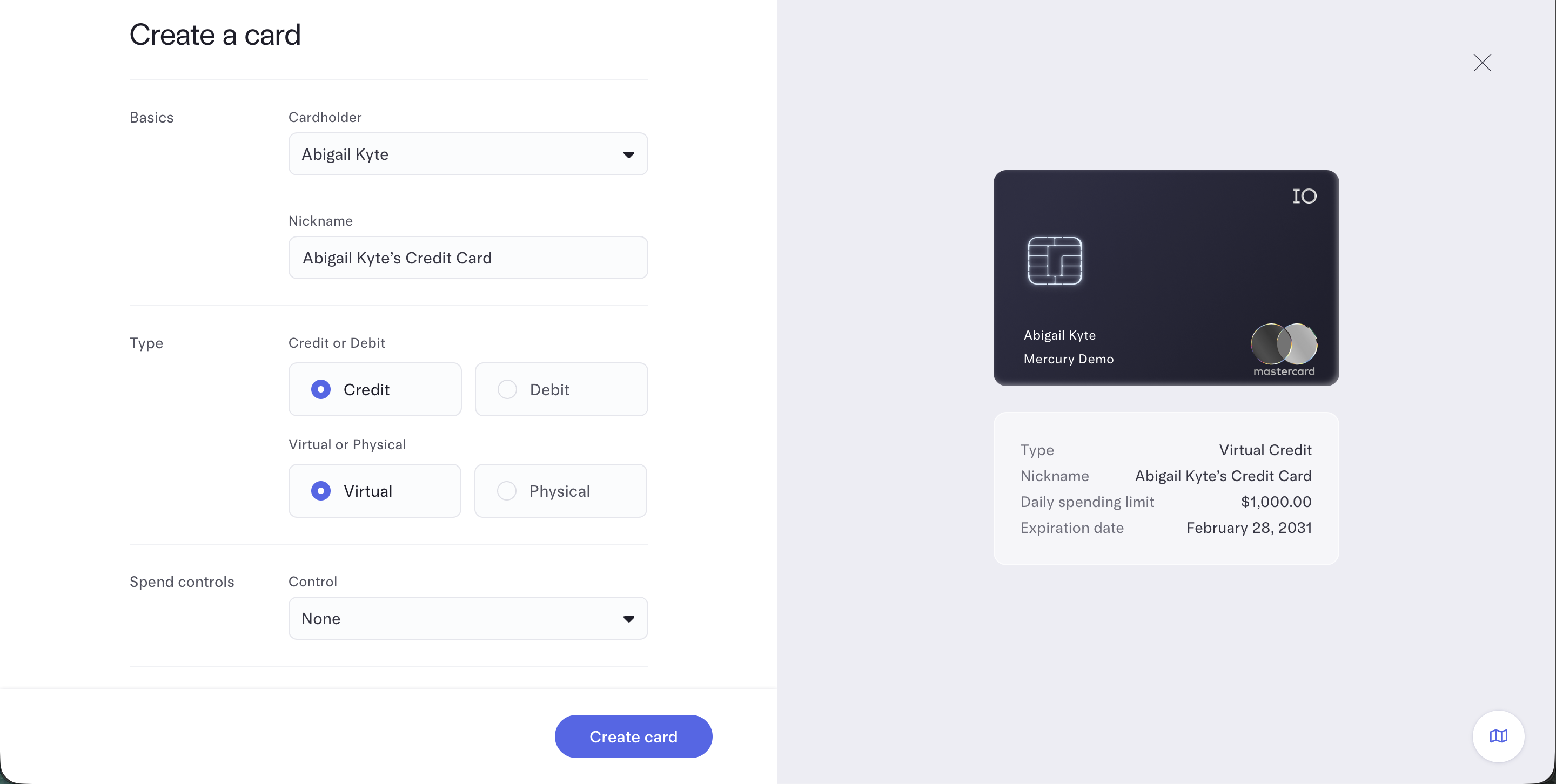

Organization & ControlsMercury is better than Novo when it comes to organizing funds and controlling how money moves. Mercury gives you true multiple checking and savings accounts (up to 100 of each per business), lets you set target balances for each, and has super flexible auto-transfer rules that actually move money between real accounts, not just virtual buckets. Novo's "Reserves" are just budgeting envelopes inside a single account, so everything stays lumped together, and you don't get any of those automated balance controls.

If you're running multiple businesses or want to handle personal banking too, Mercury lets you manage everything under one login and even gives your team personal accounts for free. Novo makes you juggle separate logins for each business, which gets annoying fast.

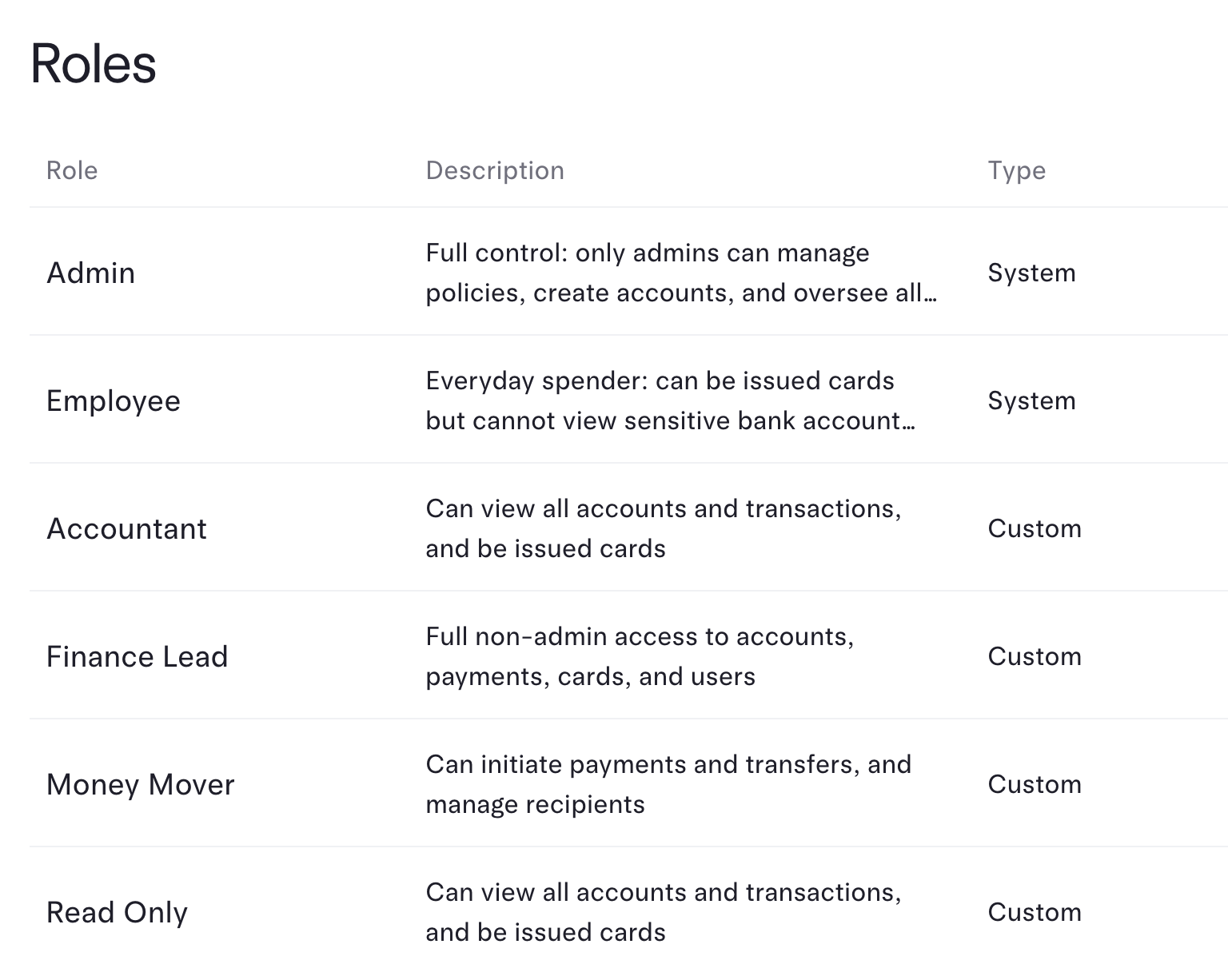

The biggest deal breaker: Mercury lets you set detailed user roles and approval workflows (like dual admin approvals, view-only roles, and payment thresholds), so you can actually control who sees and moves money. Novo only offers full-access; anyone you add can do anything, with zero guardrails or partial permissions. That's a huge risk for any team.

Unless you're a solo founder who never needs to delegate or separate funds beyond basic envelopes, Mercury is the clear pick. The gap in control and organization is massive.

User Experience

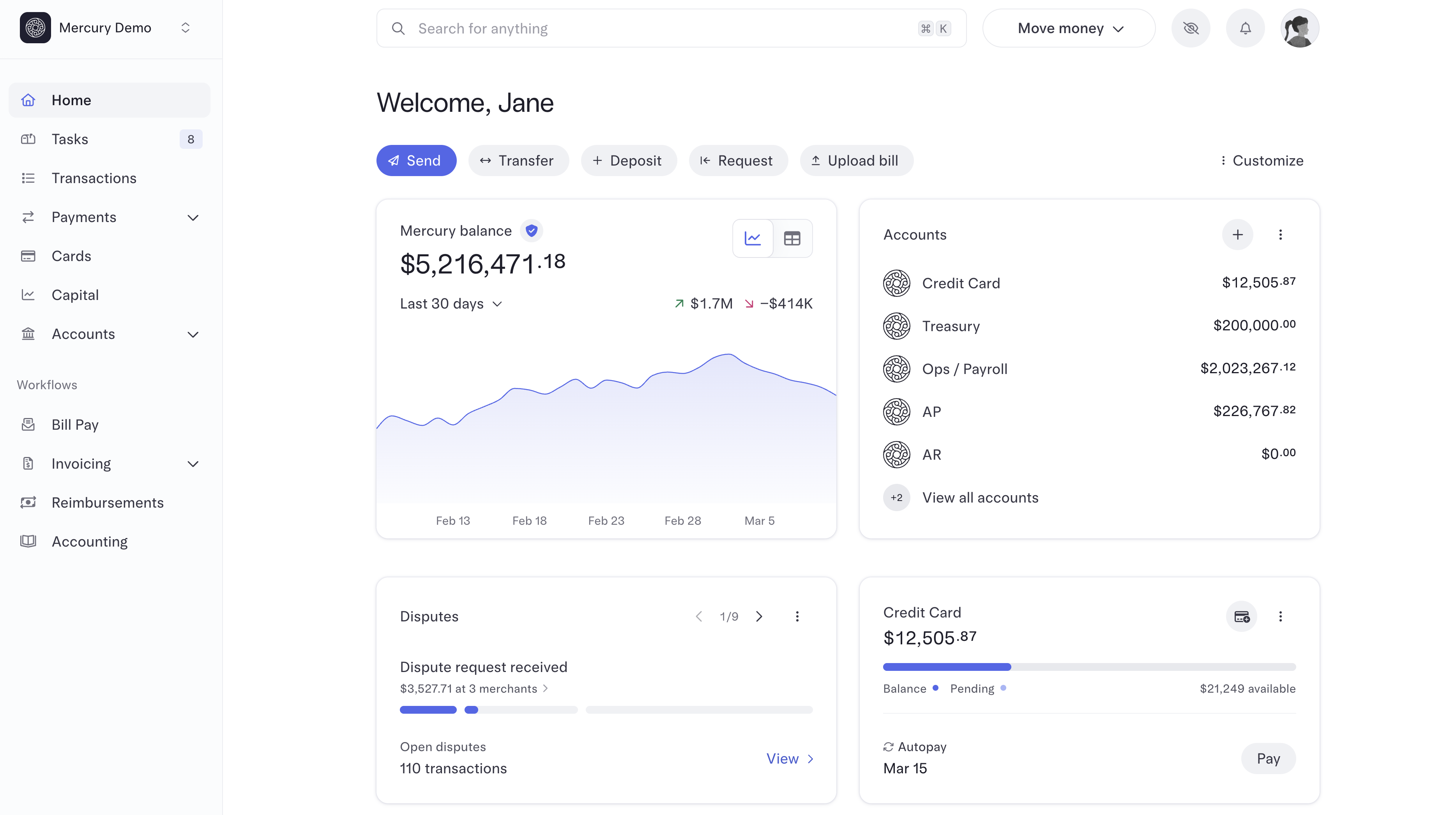

User ExperienceMercury Bank is in a different league for user experience. Its interface is modern, smooth, and gets called out as one of the best by users and reviewers alike. Every part of using it feels intuitive and just works, to the point where people don't want to switch after trying it.

Novo's interface is simple and usable, but it doesn't match Mercury's thoughtfulness or polish. If you want speed, clarity, and a banking app that actually feels good to use, Mercury is the obvious pick. Novo is fine, but Mercury makes it feel dated.

Screenshots

Screenshots

Mercury