Comparison Summary

Comparison SummaryRamp fixes annoying expense reporting and card headaches for businesses with at least $25K in the bank, while Novo is just a simple checking account for freelancers or very small businesses and doesn't handle growth well.

Only use Novo if you're a solo operator who just needs somewhere to park cash; use Ramp for anything bigger or if you hate clunky finance tools.

Ramp

RampBest if you've limited banking needs and already using Ramp

Best if you've limited banking needs and already using Ramp Novo

NovoSimple and least powerful

Simple and least powerful

At a Glance

At a GlanceComparison Video

Comparison VideoWhy We Switched to Mercury (After Testing Every Business Bank)

Why We Switched to Mercury (After Testing Every Business Bank) 8:47

8:47Why We Switched to Mercury (After Testing Every Business Bank)

Why We Switched to Mercury (After Testing Every Business Bank)Editor's Verdict

Editor's VerdictSafety & Protection

Safety & ProtectionRamp goes further than Novo when it comes to safety and protection. Ramp spreads your deposits across multiple banks for multimillion-dollar FDIC coverage, while Novo just sticks to standard FDIC insurance at one bank, capped at $250K. Novo is built for small balances and doesn't add any extra layers of protection beyond what every basic checking account offers.

Ramp also gives you more control over external ACH debits, letting you set trusted vendors or require approval on outside pulls. The catch is, even with approval required, the debit might still hit your account before it's reversed, so it's not perfect. Still, these controls are a clear step up from Novo, which only offers basic monitoring and a dispute process after something happens.

If safety and protection are your top concern, especially if you're holding more than $250K or want better control over who can pull money from your account, Ramp is the stronger pick. Novo is fine for small, simple accounts but doesn't give you the extra protection or controls that Ramp does.

Earning Interest

Earning InterestRamp actually lets you earn yield on idle cash by moving funds into government money market funds or short-term fixed income portfolios, even if it feels more like a treasury add-on than a seamless banking feature. Novo, on the other hand, gives you no way to earn interest at all, no savings account, no treasury product, and their business checking pays nothing.

If earning interest is important, Ramp is the only real option here. Novo just can't do it. Even though Ramp's setup isn't as smooth as some dedicated banking platforms, at least you have a path to put idle cash to work. Go with Ramp if you want your business funds to earn something.

Money Movement

Money MovementRamp edges out Novo for money movement, mainly because it covers the basics for managing vendor payments, ACH, wires, and checks pretty smoothly. You can handle your daily payments without a hitch, and it's set up to do exactly what most businesses need right out of the gate.

Novo, on the other hand, feels a lot more limited if you're actually running a business that needs to pay vendors regularly. There's no self-service onboarding for vendors, no built-in way to collect tax info like W-9s, and no automatic invoice scraping. Even sending checks gets clunky if you need to include forms, so it's not great for anything more complicated than very simple payments.

If you just need to pay a contractor here and there, Novo might be fine. But for a business that needs reliable, straightforward vendor payments and the basics handled, Ramp is the better pick. Just know that Ramp isn't a full banking replacement and most teams use it alongside a real business bank, but for the money movement piece alone, it's clearly ahead of Novo.

Organization & Controls

Organization & ControlsRamp gives you real user roles and approval controls, while Novo just doesn't. With Novo, anyone you add gets full, owner-level access, so if you need guardrails or even basic read-only permissions, Novo is a non-starter for teams. Ramp lets you limit access, assign roles, and set up payment approvals, so you actually have a way to control who can see and move money.

On the account structure side, Novo's Reserves are just internal buckets, not real accounts, and all the money stays in one checking account. You can auto-allocate deposits into these buckets, which helps with simple budgeting, but you don't get true sub-accounts, target balances, or separate cards per bucket. Ramp isn't great here either, it doesn't do envelope budgeting or let you set up lots of true bank accounts. But you can at least manage multiple entities under one login, and you get some automation to keep balances at target levels or sweep funds out to investments.

If you're solo and just want simple budget buckets, Novo's Reserves are a bit more straightforward. But as soon as you need real controls, team safety, or basic approval workflows, Ramp is the only practical option here. Neither is perfect for full banking automation, but Ramp is the safer, more controlled choice if you have a team or care about limiting who can move money.

User Experience

User ExperienceRamp feels faster and more modern right away, thanks to its slick interface and universal search. It's easy to find what you need quickly, which gives it a noticeable edge if you care about speed and clarity.

But Ramp's banking interface takes a back seat to its expense management tools. Most of the sidebar is focused on expenses, so the banking experience isn't front and center. If you only want banking, this can make things feel a bit cluttered.

Novo keeps things simple, but its interface isn't as modern or thoughtfully designed as Ramp's. It's straightforward and gets the job done, but it doesn't stand out for speed or clarity.

If you want the best user experience for business banking specifically, Ramp is a bit better, just know you'll be working in a tool that's really built for expense management, not banking first. Novo is fine, but Ramp's interface is cleaner and easier to use for most things related to banking.

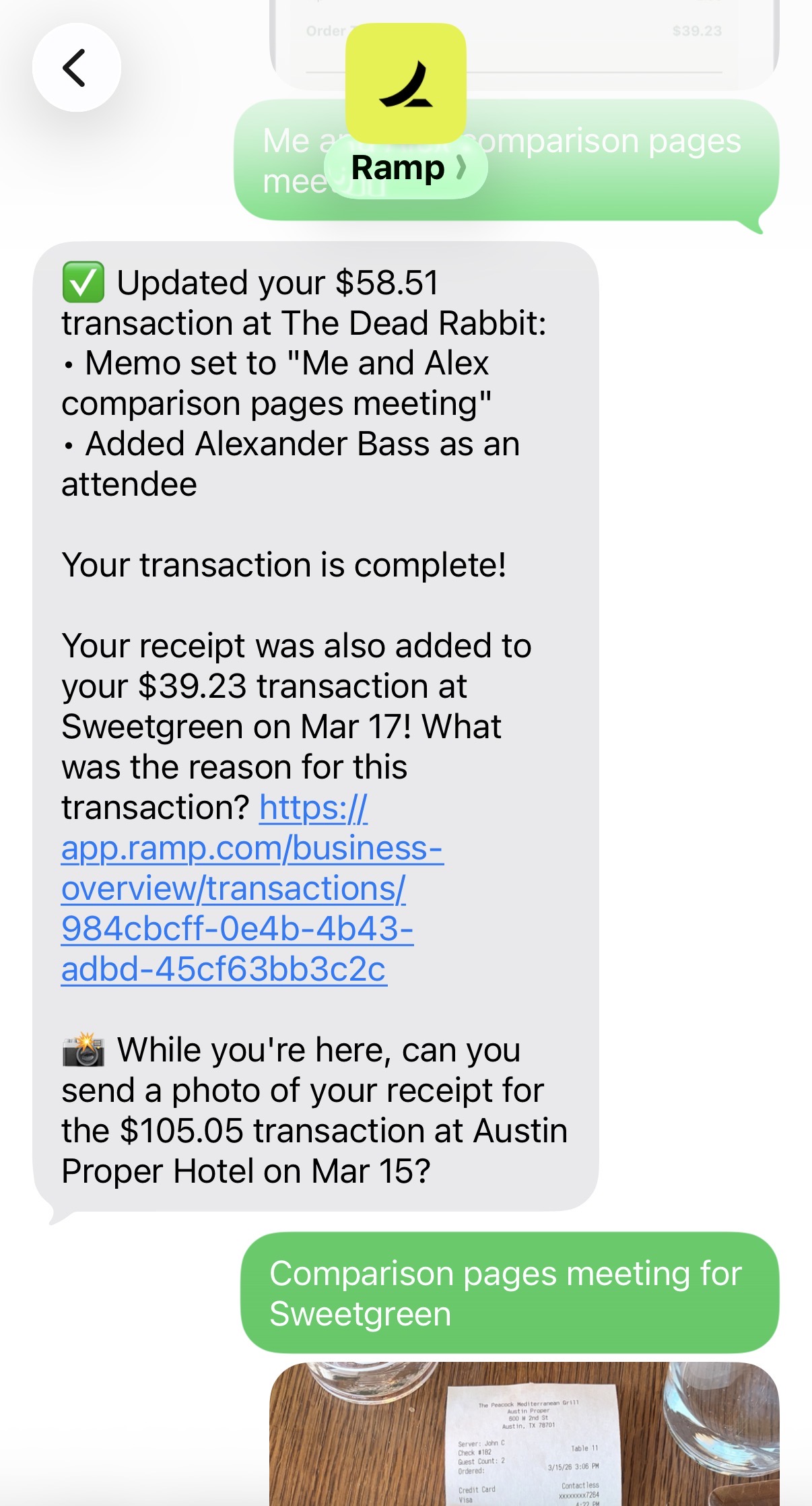

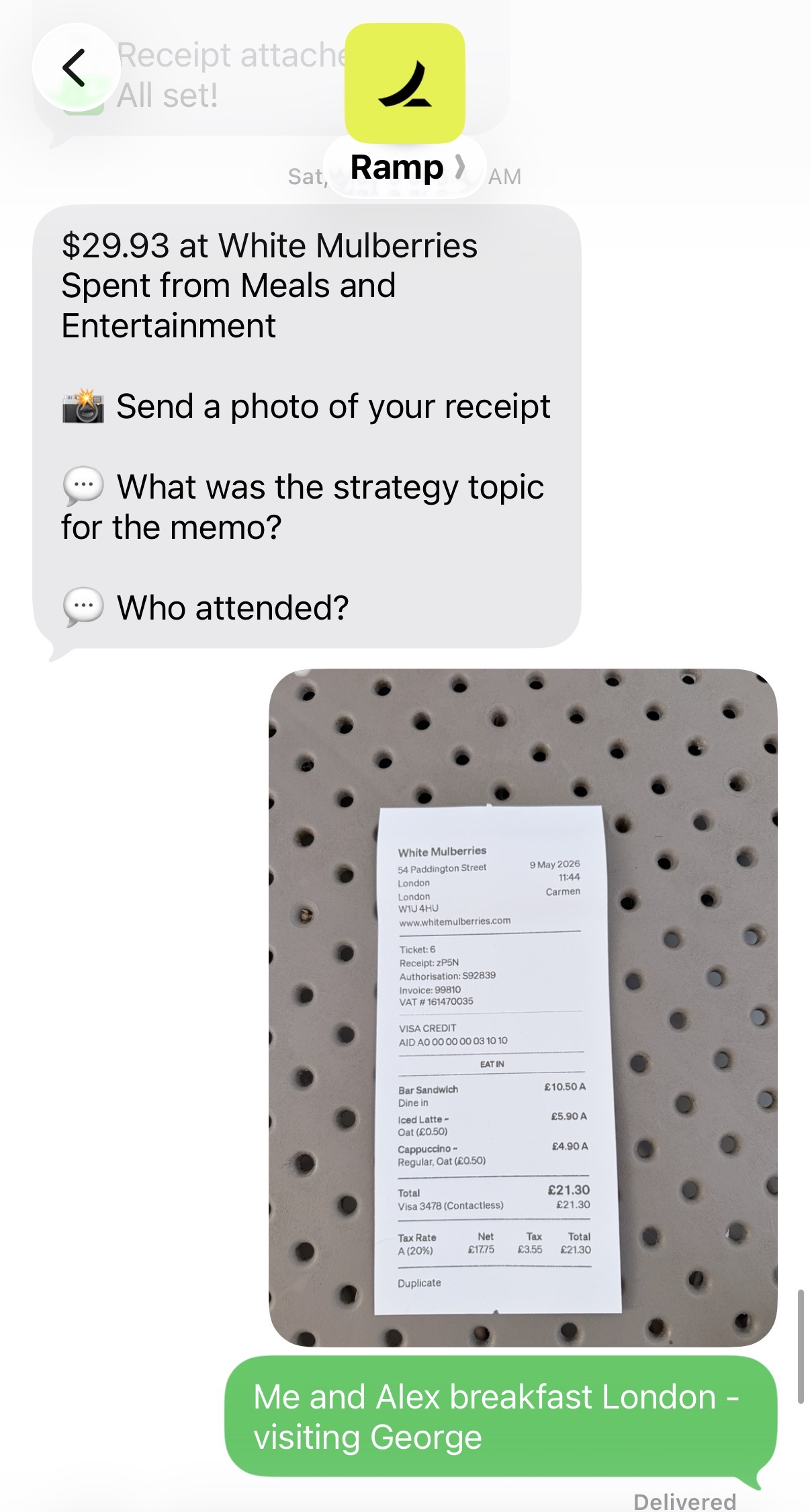

Screenshots

Screenshots

Ramp